When you prepare IFRS financial statements, you need to present some items in other comprehensive income, some items in profit or loss and some items in changes in equity.

Sometimes it’s not that clear what comes where and many finance people make serious mistakes – and yet these mistakes could be prevented so easily!

What items belong to OCI? And what items belong to P/L?

What is the difference between other comprehensive income and profit or loss? And what is the difference between other comprehensive income and changes in equity?

The whole thing becomes clear when you focus on the net assets. Net assets are simply total assets less total liabilities of a company. It is the same as equity which is the residual interest in the assets of an entity after deducting all of its liabilities.

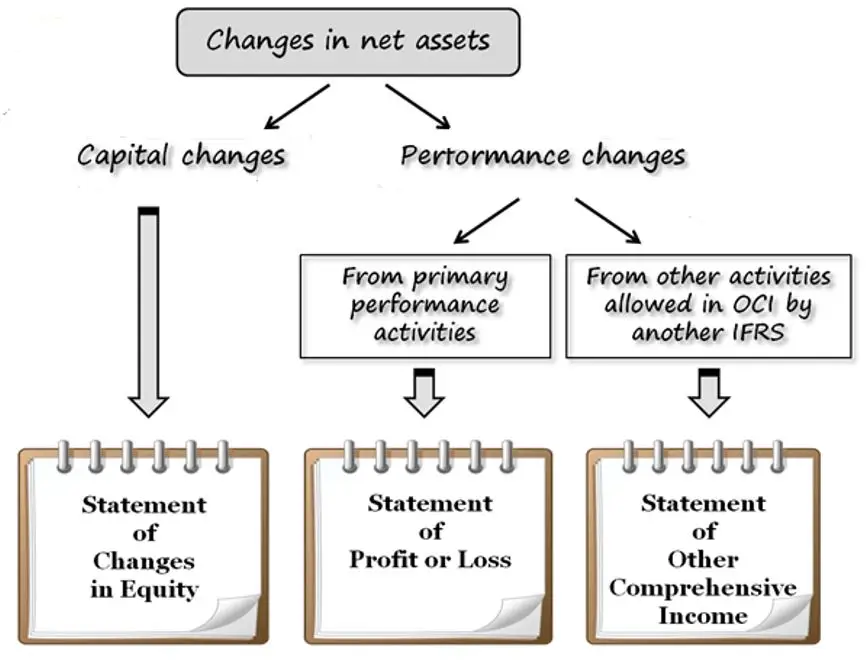

What items belong to net assets?

Basically it is share capital, share premium, reserves, retained earnings or losses and some other items, too.

What can cause the change in net assets?

Net assets or equity can increase or decrease as a result of several things, for example:

- Shareholders loan

- Capital Increase

- Profit or loss for the period

- Treasury stock

- Pays out dividends to shareholders

- Revaluation of certain assets directly through equity and not through profit or loss

The key to understand the difference between profit or loss, other comprehensive income and changes in equity is to understand where these changes are coming from.

Which statement to use?

We can classify changes in net assets or equity into 2 main categories:

- Capital changes – these are all changes related to introduction and return of capital to shareholders, such as:

- Issuance of new shares

- Paying out of dividends to shareholders

- Buy-back of own shares from the market

- Performance changes – these are all changes coming from the activities of the company and not from the shareholders.

We can further divide this category into 2 subcategories:

- Changes resulting from or related toprimary performance or main revenue-producing activities of the company that are reported in profit or loss such as:-

- Revenue from sales of goods or services

- Expenses incurred to make sales of goods or services

- All other income and expenses, such as finance, administrative, marketing, personnel, etc.

- Gains related to sale of property, plant and equipment, etc.

- Changes resulting from other, non-primary or non-revenue producing activities of the company that are not reported in profit or loss as required or permitted by other IFRS standard.

- Changes in revaluation surplus related to property, plant and equipment

- Actuarial gains and losses related to employee benefit

- Gains and losses arising from translating the financial statements of a foreign operation

- The effective portion of gains and losses on hedging instruments in a cash flow hedge

- Gains and losses on remeasuring available-for-sale financial assets

One thing to note is that these items occur very rarely when it comes to small and medium-sized businesses. It means that the OCI is mainly used to value bigger corporations that encounter such financial events.